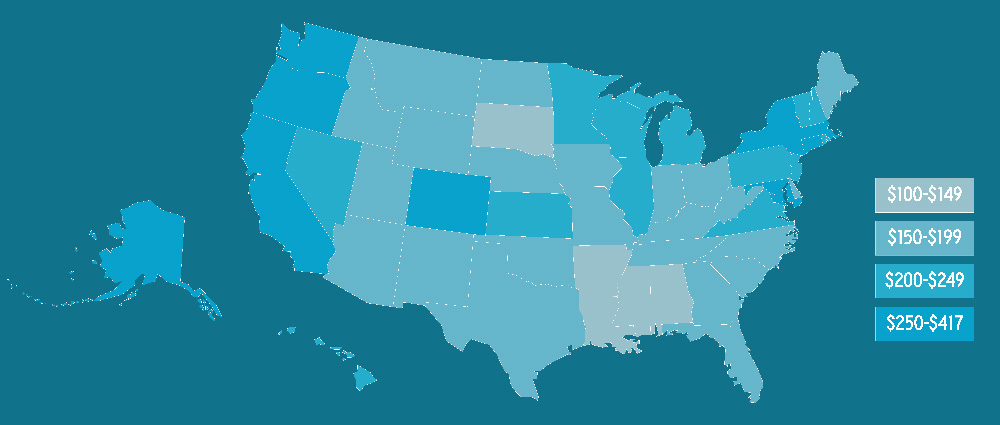

According to Care.com’s 2023 Cost of Care Report, families are spending an average of 27% of their household income on childcare expenses in 2023. The chart shows how the average weekly cost of daycare per child varies by state.

According to Care.com’s 2023 Cost of Care Report, families are spending an average of 27% of their household income on childcare expenses in 2023. The chart shows how the average weekly cost of daycare per child varies by state.

According to the FBI Internet Crime Report, Americans lost over $10.2 billion to cyber-enabled fraud, including $107 million to spoofing in 2022. Even savvy people can be caught by sophisticated schemes. Don’t be a victim; here are some common types of threats you should know about.

Spoofing is when online scammers message you, posing as a trusted vendor you know. They use email, social media, texts and other messages to lure people to fake stores that steal your money, credit card details, or personal information. Don’t click on any URL that looks slightly odd.

If your business has been spoofed, warn your customers to be on the lookout. Then, ensure that they have access to your website, email and shipping information.

You may receive a message claiming your package has been delayed and you must pay a fee to have it delivered. Think before you click.

The post office and other delivery services usually leave a note in your mailbox or at your door, rather than send a message. So, unless you expect a package and are positive that you recognize the sender, delete the message. Generally, if you are surprised by messages, or receive one that does not seem right, it is probably a scam.

With the holidays here and the end of 2023 near, I’m uncertain how much to tip the people whose services I’ve used during the year. Any guidelines?

The following chart provides suggested tipping amounts for various service providers.

Relief is here for 401(k) plan sponsors, participants and administrators. The SECURE 2.0 Act initially stated that employees aged 50 and older who earned $145,000 or more in 2023 could only make catch-up contributions to Roth 401(k) accounts in 2024 and later. However, IRS Notice 2023-63 postpones the new catch-up contribution rule for two years until January 1, 2026.

The notice also fixed a glitch in the law that inadvertently deleted part of the tax code, so it reads as if the ability for any employees to make catch-up contributions is eliminated beginning in 2024. The IRS says it will allow these catch-up contributions to be made, even though Congress did not fix this error in the law.

The IRS expects to provide future guidance saying that the mandatory Roth 401(k) catch-up provision does not apply to high-paid self-employed persons who have self-employment income instead of W-4 wages.

Scott owns a popular coffee shop. Earlier in the year, he noticed a discrepancy in stock. It turned out to be petty theft by an employee. The employee was terminated, and Scott reported the loss to his insurer, who recommended he take these steps to help prevent future losses:

Scott’s accountant also pointed out that for income tax purposes, Scott should be able to deduct any part of the loss not covered by the insurer — the deductible, for instance — if all other tax requirements are met.

Client Profile is based on a hypothetical situation. The solutions discussed may or may not be appropriate for you.

Are you thinking of selling your primary residence? Unless the home has decreased in value since you bought it, you’ll want to know about potential capital gains tax on your sale. You don’t want to incur a larger-thannecessary tax bill.

Gains on the sale of personal or investment property held for more than one year are taxed at favorable capital gains rates of 0%, 15%, or 20%, plus a 3.8% investment tax for people with higher incomes. Gains on these properties held for one year or less are taxed at higher ordinary income rates. Residential real estate is an exception.

Up to $250,000 ($500,000 for joint filers) of your gain is tax-free if you’ve owned and lived in your home for at least two out of the five years before you sell. Any gain greater than this exclusion is taxed at capital gains rates. Losses from the sale are not deductible. A spouse who sells the family home within two years after the other spouse’s death gets the total $500,000 exclusion, provided the two-out-of-five-year use and ownership tests were met before death.

If you must sell your home before two years due to job changes, illness, or unforeseen circumstances, you may still be eligible for part of the gain exclusion. The exclusion percentage that can be taken equals the portion of the two years you used the home as a residence.

Was your home damaged or destroyed in one of this year’s federally declared natural disasters? Then your capital gain amount will equal any insurance proceeds you received that exceed your pre-disaster tax basis in the home. The gain exclusion is available for this gain amount.

Home sales are complex and can be emotional. Consult your tax and real estate professionals before selling. Your financial professional can help you budget for your new home.

Looking back at 2023 may provide ideas to help get your business off to a better start in 2024. Some questions to ask yourself include:

Ensure your vision for your future business is understood by staff and help incentivize them to commit fully.

Consider resources, market share, new opportunities, challenges and potential bombshells to ensure your goals are rational and reasonable. Get input from your staff and professional advisors.

Your staff and family depend on you. The bottom line is you can’t give your best to either if you don’t care for yourself. Remember: Stress is a killer. Strive to maintain a workleisure balance.

When doing your year-end financial review, consider managing your personal finances like you handle your business. Why? Looking at your

personal situation from a business perspective helps you find places to cut expenses, boost cash flow and improve your personal financial situation.

First, summarize the current value of all your assets, including cash and cash equivalents, brokerage balances, retirement funds, real estate and your personal property. Then, subtract your liabilities. Remember that some business assets and debts may need to be included depending on your business structure.

When considering cash inflow, remember to include any dividend and interest income, rental income, etc. Compare inflow to outflow, including loan payments, food, clothing, education savings, taxes, insurance, gifts and more.

Recruit family members to assist by tracking their spending for a month — every penny. It isn’t easy, but it’s important.

Once you know where your money is going, look for spending cuts and ways to increase savings. Places many families can cut are forgotten subscriptions and extra streaming services. Fortunately, there are several apps to help with these tasks.

Like your employees, examine your benefits elections. Do they still fit your family situation? The same goes for your withholding election. Review your insurance coverage: health and disability, life, homeowners and personal-liability. Your insurance professional can help identify changes that may be needed. Make sure to regularly check your credit report, too.

Make sure you have a retirement transition plan and an updated estate plan. Review beneficiary designations for retirement accounts, insurance policies and provisions in your will and living trust to help ensure they still match your wishes. Updates are easy.

If possible, increase your retirement plan contributions each year and take full advantage of tax-deferred compounding.

Manage Family Finances Like a Business – when doing your year-end financial review, consider managing your personal finances like you handle your business.

2023 Hindsight – looking back at 2023 may provide ideas to help get your business off to a better start in 2024.

Understanding Capital Gains Tax On Home Sales – are you thinking of selling your primary residence.

Roth 401(k) Contribution Reprieve – IRS notice 2023-63 postpones the new catch-up contribution rule until January 1, 2026.

December 2023 Question and Answer

Beware of Holiday Scams – even savvy people can be caught by sophisticated schemes.