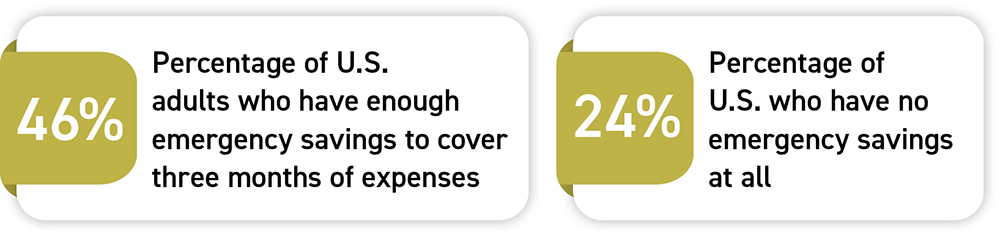

With the holidays behind us, it’s a good time to review your savings and get back on track, especially if you had to dip into your emergency fund during the holidays. Having an emergency fund is key to ensuring funds are available when unexpected financial hardships occur. Aim to save 3-6 months’ worth of living expenses to give yourself peace of mind.

PUT IT IN WRITING

For many people, writing it down makes saving money for an emergency fund real, not theoretical. Talk with your loved ones to discuss how much you need and solicit ideas for finding the extra dollars that can add up over time. Make a chart and track how much you’re able to save each month toward your goal.

SHOW ME THE MONEY

Whether part-time gigging or selling unwanted items via the Internet or smartphone apps, you can potentially increase your disposable income — and your emergency funds — quickly. The same thing goes for raises and bonuses from work. Keep your car for an extra year or two to go without monthly car payments. Keep your phone, too, with new smartphone prices soaring.

MAKE SMALL SACRIFICES

Passing on one $5 designer latte, one $10 lunch, and one $75 dinner every two weeks is another way to quickly increase your funds.

MAKE BIGGER SACRIFICES

Still looking for free money to increase your emergency funds? Maybe you need to free it up by first creating a budget that includes your income and itemized expenses. Little adjustments add up. Scour your phone and cable bills to eliminate unneeded services. Study your clothes and grocery bills to find additional savings. Write down every dime you spend to get the best idea of where your money goes.