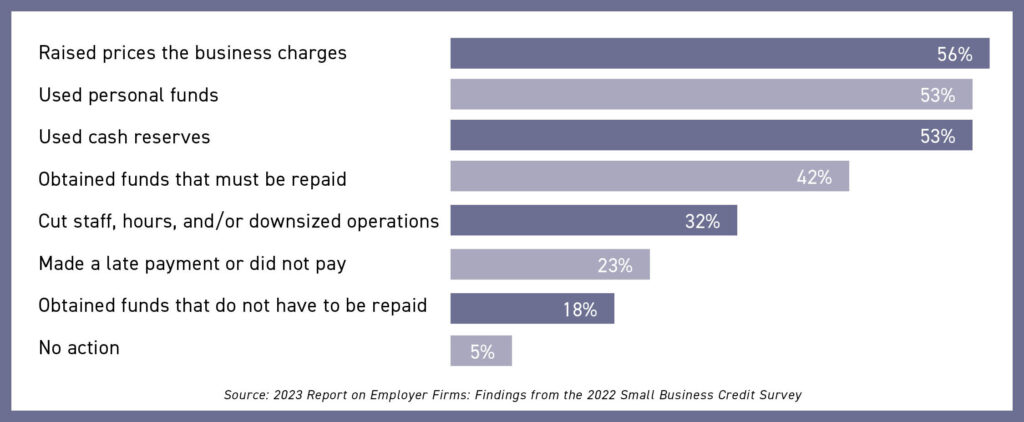

Prior 12 Months (% of employer firms with financial challenges)

Raised prices the business charges – 56% Used personal funds – 53% Used cash reserves – 53% Obtained funds that must be repaid – 42% Cut staff, hours, and/or downsized operations – 32% Made a late payment or did not pay – 23% Obtained funds that do not have to be repaid – 18% No action – 5%

Source: 2023 Report on Employer Firms: Findings from the 2022 Small Business Credit Survey

Everyone’s goal should be an excellent personal and business credit score. Here’s some simple guidance on how you may be able to improve yours.

Pay your bills on time. According to credit agencies, your credit history is the most influential factor in determining your credit score. Also, keep track of your credit balances versus your credit lines. Some experts recommend a 10% credit utilization as ideal.

The recommendation to keep open credit accounts you’ve paid off ties into this utilization guide by maximizing your credit lines. How many accounts you have and how long they’ve been open are essential factors in your score. The longer you’ve had an account, the better. Another important tip is to not jump on credit offers you receive to see if you get approved. Make sure you need the credit before you apply because each application you make can lower your credit score. Finally, periodically monitor your credit scores and be patient. Newly established good credit habits may take a while to show up in your numbers.

A digital or online presence has become a part of daily life for most people. That digital presence also should be a part of your estate plan. If it isn’t, here’s how to get things together to include those assets in your planning.

First, list your electronic and virtual accounts and assets, including account names, usernames and passwords. Review and update periodically. Things to include:

Email accounts (personal and business)

Online banking accounts

Social media accounts

Photos and text, graphic, and audio files stored on your computer or in the cloud

Cellphone apps

Utility accounts

Loyalty program benefits such as credit card rewards

Online store accounts

Gaming accounts

Cryptocurrency keys

E-commerce accounts

Domain names, including blogs

Your professional advisor can help ensure you’ve listed all your digital assets and advise you on the next step, which is to decide how you want your digital assets handled. Most social media companies have specific policies for accessing and dealing with deceased members’ accounts. Other companies may as well, with some allowing you to authorize a person to access your digital account and some prohibiting the transfer of digital assets to another person or account. Knowing the policies for all of your accounts is imperative to direct how you want them handled.

Next, pick a digital executor. Weigh whether your named estate executor is the logical choice or if someone else—a family member or close friend—would be a better choice for your digital assets. Make sure your choice (or choices) understand their tasks and responsibilities before they accept the designation. You can refer to your digital assets document and name a digital executor in your traditional will.

There’s good news for you and your employees if you offer a high-deductible health plan (HDHP) and health savings accounts (HSAs). In one of the largest jumps in recent years (7.8%), the HSA contribution limits for 2024 will rise to $4,150 (from $3,850 in 2023) for employees with single health plan coverage and to $8,300 (from $7,750) for those with family coverage. Workers aged 55 and older can contribute an extra $1,000 (unchanged from 2023). So an older married couple will be able to contribute $10,300 in 2024.

Your high deductible health care plan will qualify if the 2024 annual deductible is at least $1,600 for self-coverage or $3,200 for family coverage.

Employee out-of-pocket expenses (deductibles, copayments, coinsurance, and some uncovered services) cannot exceed $8,050 (self-only) or $16,100 for family coverage.

Our engineering firm could use new office furniture. Is now a good time to buy?

ANSWER:

The third quarter of the year isn’t the best time to purchase office furniture if you’re watching costs. Generally, the furniture industry releases new models twice a year – in the spring and fall. It would be best to buy new furniture in the off-season to get your best deals. Some better times:

January: Vendors may discount 2023 furniture to make way for 2024 models.

April-May: For furniture retailers, Memorial Day sales rival Black Friday sales.

August: Back-to-school shopping deals can expand to include furniture.

Okay, so you’ve decided to sell your business and retire (or for another well-throught-out reason). You’ve discussed it with your family, and everyone is on board. You don’t want any family glitches to delay and possibly torpedo a sales deal you work out. So, what’s next?

Put together your sales team: your accountant, an attorney experienced in business transactions, and a business broker

Have your business evaluated.

Develop an exit plan if you haven’t already.

Come up with an idea of your “perfect” buyer and share it with your broker before you sign the legally binding contract to list the business for sale.

Provide the broker with detailed information about the business: history, product/service mix, organizational chart, growth opportunities, and anything else you think is of value to potential buyers.

Prepare for due diligence: gather your past three years financials, contracts, and licenses and prepare a disclosure statement. Your professional advisors can help with other items that may be needed.

Do any maintenance, painting, cleaning, and other sprucing up to improve the physical appearance of your business.

The Taylor brothers have enjoyed the good fortune of seeing their family heating and cooling business grow steadily. But that growth has sparked concerns about being liable for alternative minimum tax (AMT) in 2023.

Small businesses that qualify for small-business corporation status avoid the AMT’s potential liability and the administrative burden of calculating the tax. The Taylors can use the following gross-receipts test to see if their business qualifies. A small-business corporation is defined as having a three-year average annual gross receipts not exceeding $5 million for its first tax year and not having three-year average annual gross receipts exceeding $7.5 million for any later year.

More simply, the Taylors don’t need to worry about being liable for AMT as long as their business’s average gross receipts for all three tax-year periods ending before the current tax year are $7.5 million or less. For additional details or questions, they should contact their professional advisor.

Client Profile is based on a hypothetical situation. The solutions discussed may or may not be appropriate for you.

With new hires, you want to be confident that they will become loyal, productive, and valuable long-time employees. One way to achieve this goal is to have a well-thought-out employee benefit program that serves your needs. To see if your program has gaps you may want to consider what competitors offer and what employees look for.

According to a recent study*, business owners are offering benefits at the highest rates since 2008. What benefits are owners ramping up? The percentage of employers offering comprehensive health insurance, health savings accounts, wellness solutions, and employee assistance programs (EAPs) increased from 2022 to 2023. As for qualified retirement plans, the popularity of 401(k) and Simple IRA plans increased among employers, while other plans were offered at about the same rate as last year. For supplementary key employee benefits, both disability income insurance and deferred compensation dropped in popularity among employers while other benefits remained steady.

Still, affordability remains businesses’ top priority where benefits are concerned, ahead of attracting and retaining qualified employees and staff productivity. Your goal in reviewing your benefits program should be working with your professional advisor to achieve quality benefits at a reasonable cost to your business.

On that note, some of the “benefits” employees are looking for can be provided at little or no cost. Another study** found that most workers judge whether a job is good by the pay, boss, health and retirement benefits, vacation time, friendliness of co-workers, whether they’re helping people or society, remote work options, and opportunities for advancement. Pay was the top consideration at 45% of employees, followed by a good boss at 14%. People ages 27 to 34 are more likely to say promotion opportunities and advancement are important than older employees. And they place less emphasis on health insurance, retirement, and vacation benefits.

* 2023 Report on Employer Firms: Findings from the 2022 Small Business Credit Survey ** Washington Post-Ipso Poll, 2023